Business Insurance Agent In Jefferson Ga Fundamentals Explained

Table of ContentsNot known Facts About Business Insurance Agent In Jefferson GaThe Only Guide to Life Insurance Agent In Jefferson Ga9 Easy Facts About Insurance Agent In Jefferson Ga ShownA Biased View of Home Insurance Agent In Jefferson Ga

Discover more concerning just how the State of Minnesota supports active duty members, professionals, and their families.

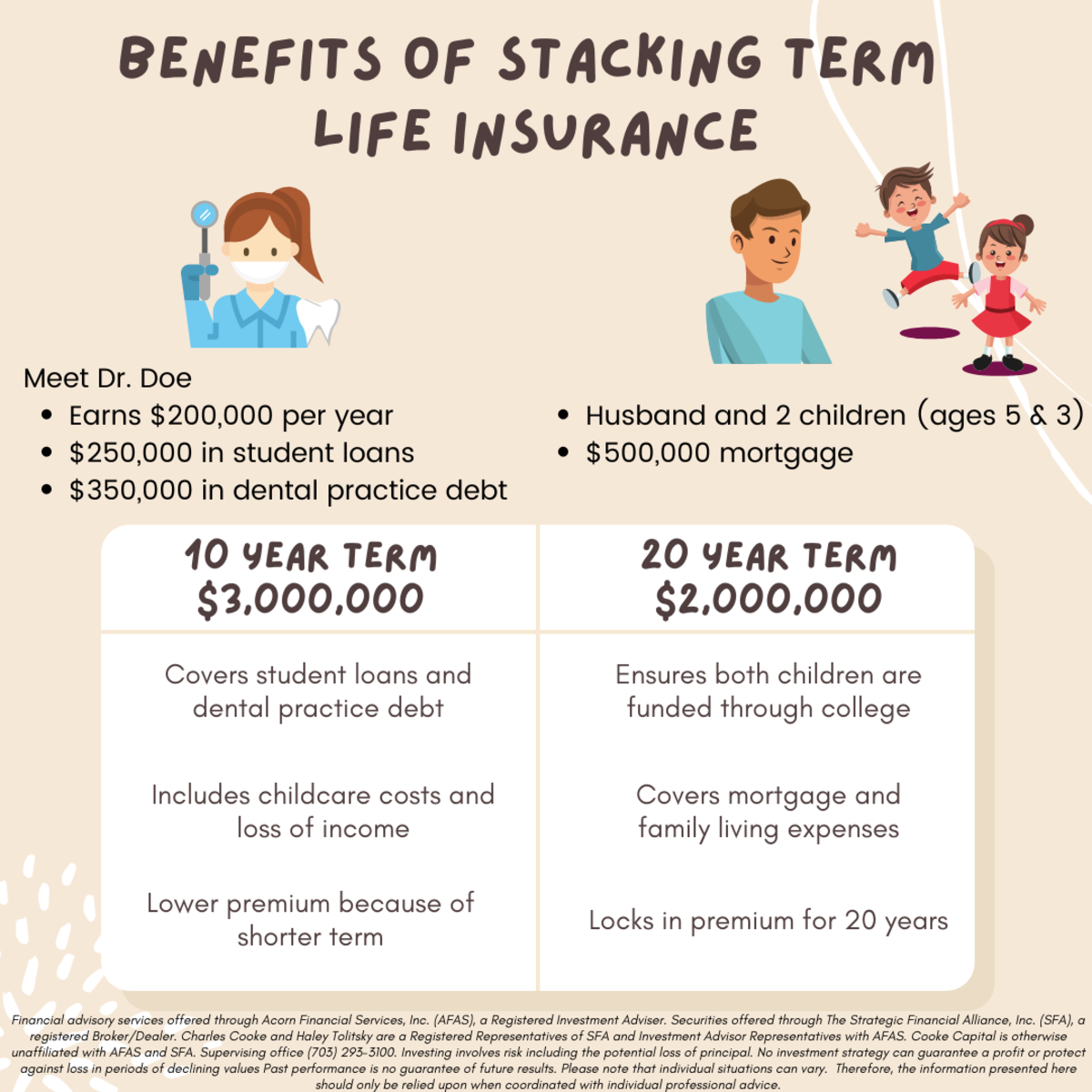

Term insurance policy provides defense for a given amount of time. This period can be as short as one year or provide coverage for a specific number of years such as 5, 10, twenty years or to a defined age such as 80 or sometimes as much as the oldest age in the life insurance coverage mortality.

The longer the warranty, the higher the preliminary costs. If you pass away throughout the term period, the firm will certainly pay the face quantity of the plan to your recipient. If you live past the term duration you had actually picked, no advantage is payable. Generally, term plans supply a death benefit with no cost savings element or money worth.

Rumored Buzz on Business Insurance Agent In Jefferson Ga

The costs you pay for term insurance coverage are lower at the earlier ages as contrasted with the costs you spend for irreversible insurance, but term rates increase as you get older. Term plans might be "convertible" to a long-term plan of insurance. The coverage can be "level" providing the exact same benefit till the plan ends or you can have "reducing" insurance coverage throughout the term period with the costs staying the same.

Presently term insurance rates are really competitive and amongst the most affordable traditionally skilled. It must be noted that it is a commonly held belief that term insurance coverage is the least expensive pure life insurance policy protection offered. https://www.twitch.tv/jonfromalfa1/about. One needs to evaluate the policy terms meticulously to choose which term life alternatives are ideal to satisfy your certain scenarios

The length of the conversion period will differ depending on the kind of term policy acquired. The premium price you pay on conversion is generally based on your "current attained age", which is your age on the conversion date.

Under a level term policy the face quantity of the plan continues to be the very same for the whole period. Commonly such policies are sold as mortgage security with the quantity of insurance decreasing as the balance of the mortgage lowers.

The Ultimate Guide To Business Insurance Agent In Jefferson Ga

Commonly, insurers have not can change premiums after the policy is offered. Since such plans might proceed for years, insurance providers need to utilize conservative death, rate of interest and expenditure rate estimates in the costs computation. Adjustable premium insurance, nevertheless, permits insurance companies to supply insurance coverage at reduced "present" costs based upon less conventional assumptions with the right to alter these costs in the future.

In some cases, there is no relationship in between the size of the cash money worth and the Resources premiums paid. It is the cash value of the plan that can be accessed while the policyholder lives. The Commissioners 1980 Requirement Ordinary Mortality (CSO) is the current table utilized in determining minimal nonforfeiture values and policy books for common life insurance policies.

The plan's important elements include the premium payable annually, the death advantages payable to the recipient and the cash money abandonment value the policyholder would certainly get if the plan is given up before death. You might make a financing versus the cash worth of the policy at a defined rate of rate of interest or a variable interest rate but such outstanding financings, if not paid back, will certainly decrease the survivor benefit.

The Only Guide to Life Insurance Agent In Jefferson Ga

If these price quotes change in later years, the company will certainly change the premium accordingly however never ever over the optimum guaranteed premium specified in the plan. An economatic whole life policy gives for a basic amount of getting involved entire life insurance policy with an extra supplementary insurance coverage supplied with using rewards.

Ultimately, the dividend additions need to equate to the initial amount of supplementary coverage. Due to the fact that rewards may not be enough to buy adequate paid up additions at a future date, it is feasible that at some future time there might be a significant decrease in the quantity of extra insurance coverage - https://www.behance.net/jonportillo1.

Due to the fact that the premiums are paid over a shorter span of time, the costs repayments will certainly be greater than under the entire life plan. Single costs whole life is limited repayment life where one huge premium payment is made. The policy is completely paid up and no further costs are called for.